AU Small Finance Bank Universal Bank Transition Road to Status – RBI Approval, Compliance & Strategy

AU Small Finance Bank’s Universal Bank Transition Explained

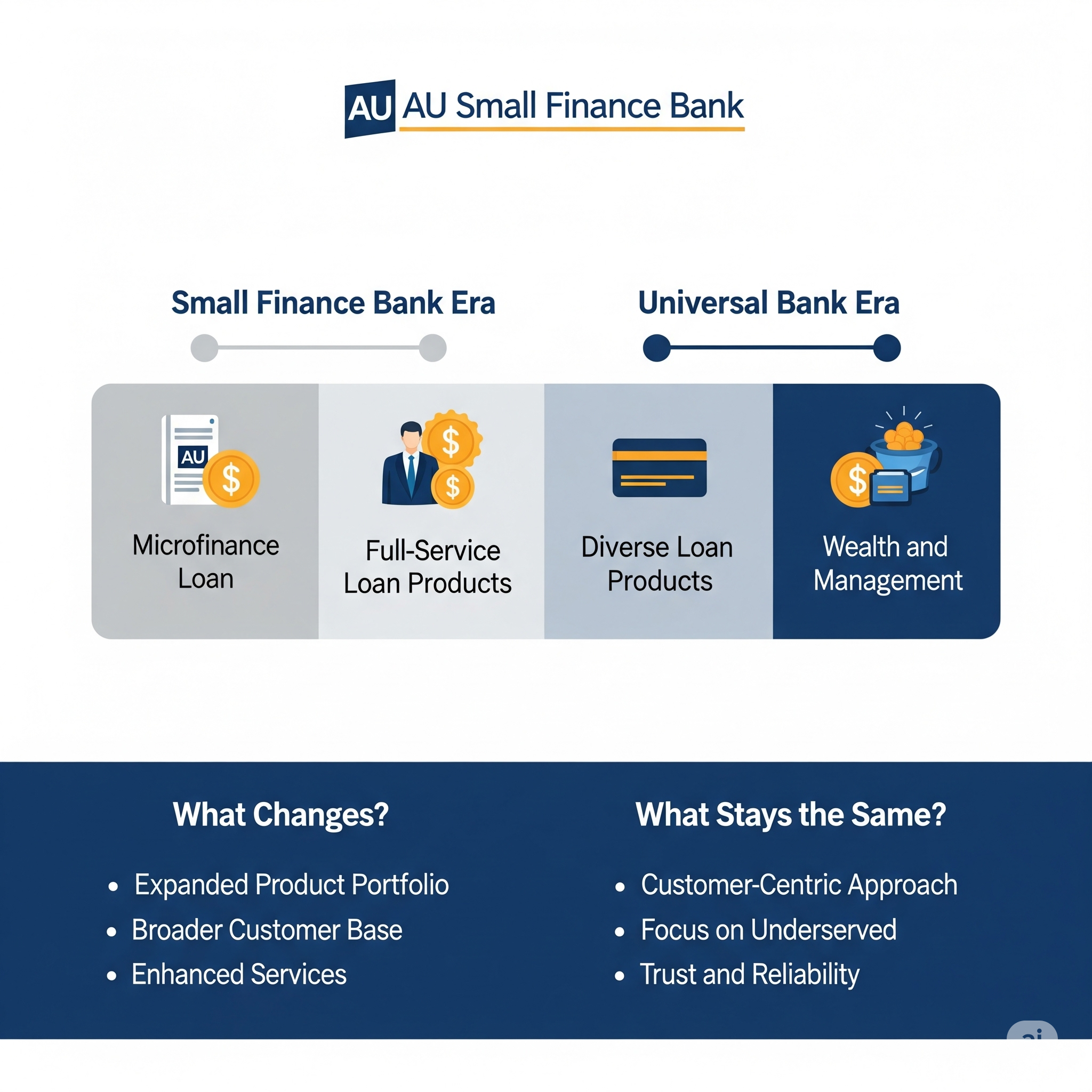

Executive Summary / Key Highlights

- RBI Approval: AU Small Finance Bank (AU SFB) has received in-principle RBI approval to transition into a universal bank.

- Compliance Deadline: The bank must restructure within 18 months, creating a Non-Operating Financial Holding Company (NoFHC) and rebranding.

- Founder’s Plan: Sanjay Agarwal, MD & CEO, will focus entirely on the bank until retirement, with no parallel ventures.

- Key Advantage: Universal bank status is expected to enhance customer trust and lower deposit mobilisation costs.

- Financial Strategy: Reduce cost of funds below repo rate in 5 years, grow unsecured loans to ~15% of portfolio, and protect net interest margin (NIM).

Regulatory Context – RBI’s In-Principle Approval

The Reserve Bank of India (RBI) has given AU Small Finance Bank Ltd the green light to transition into a universal bank. This is a significant milestone, as no universal bank licence has been issued in India for over a decade.

Key Regulatory Requirement:

- Establish a Non-Operating Financial Holding Company (NoFHC) – mandated to separate ownership from banking operations, ensuring independence and avoiding conflicts of interest.

- Complete compliance within 18 months from the date of approval.

AU Small Finance Bank Universal Bank Transition – Precondition of NoFHC Structure

A Non-Operating Financial Holding Company is a holding entity that owns the bank but does not undertake any other financial activity.

Regulatory Objective:

- Maintain governance separation between promoters and banking operations.

- Facilitate regulatory oversight across group entities.

Implications for AU SFB:

- Sanjay Agarwal’s shareholding will be shifted to the NoFHC.

- Potential tax implications – but regulatory provisions allow certain dispensations.

- The bank will work with RBI to iron out the transition process.

AU Small Finance Bank Universal Bank Transition – Rebranding Plans

The bank plans to drop the “Small Finance” tag and rebrand as AU Bank Limited.

Reason:

- Public perception challenge – many depositors don’t understand the difference between an SFB and a universal bank.

- Universal bank status signals full-service banking capabilities and can enhance trust, leading to lower deposit rates.

AU Small Finance Bank Universal Bank Transition – Impact on Customer Perception

- Brand Trust: Easier to attract deposits at competitive rates.

- Lower Cost of Funds: Current SFB deposit rates are ~100 basis points higher than universal banks.

- Market Expansion: Ability to compete with large banks for high-value clients.

- Diversified Product Range: More scope for unsecured lending, credit cards, and personal loans.

Financial Targets & Lending Strategy

Cost of Funds:

- Q1 FY26 – 7.08% (down from 7.14% in Q4 FY25).

- Target – below repo rate within 5 years.

Loan Book Strategy:

- Current unsecured loans: ~8% of portfolio.

- Cap on unsecured loans: ~15%.

- Measured expansion in personal loans and credit cards, mindful of asset quality risks.

Yield on Advances:

- Q1 FY26 – 14.1% (down from 14.4% in Q4 FY25).

- Yield likely to moderate as portfolio grows and pricing becomes more competitive.

Net Interest Margin (NIM):

- Q1 FY26 – 5.4% (down from 6.0% YoY).

- Long-term aim: Protect NIM while maintaining ROA around 2%.

Competitive Positioning

- AU’s current model – higher deposit rates and higher lending rates – positions it closer to NBFC competition than large banks.

- With universal bank status, AU plans to make loan pricing more competitive while retaining its high-yield niche markets.

- Focus remains on secured lending segments that have historically delivered stable yields.

Governance & Leadership Outlook

- RBI caps private bank CEOs’ tenure at 15 years.

- Sanjay Agarwal is in his 8th year as MD. He intends to request 15 years from the date of universal bank licence, though he expects RBI may count from SFB conversion in 2017.

- He plans to remain fully committed to the bank until retirement, exploring other ventures only afterward.

Challenges in Transition

- Structural Complexity: Setting up NoFHC and migrating shareholding.

- Tax Implications: Need for regulatory dispensation to avoid significant costs.

- Cultural Shift: From SFB focus to universal bank competitive landscape.

- Deposit Repricing: Aligning deposit rates with universal bank norms without losing customers.

Compliance Roadmap (18 Months)

| Timeline | Milestone |

|---|---|

| 0–3 months | Formalise NoFHC framework with RBI. |

| 3–6 months | Transfer promoter shareholding to NoFHC. |

| 6–12 months | Begin rebranding process to AU Bank Limited. |

| 12–15 months | Adjust product pricing strategy for universal bank positioning. |

| 15–18 months | Final RBI compliance review and full licence conversion. |

Conclusion

The RBI nod is only the first step. Over the next 18 months, AU SFB’s transformation into AU Bank Limited will depend on seamless regulatory compliance, brand repositioning, and cost-of-funds optimisation.

📢 At Estabizz Fintech, we assist BFSI players with RBI licensing compliance, NoFHC structuring, and governance frameworks.

50+ FAQs on AU Small Finance Bank’s Universal Bank Transition

A. Regulatory Approval & Licensing

1. What is a universal bank in India?

A universal bank is a full-service commercial bank that can offer a wide range of financial services, including deposit accounts, loans, investment products, and corporate banking, without the operational limitations of a small finance bank (SFB).

2. Has AU Small Finance Bank received a universal bank licence?

AU SFB has received in-principle approval from the RBI to transition into a universal bank, but the final licence will be granted only after meeting certain compliance requirements.

3. What does “in-principle approval” mean?

It is RBI’s conditional approval, allowing a bank to start the process of meeting all regulatory prerequisites before the final universal bank licence is issued.

4. What is the main precondition for AU SFB to become a universal bank?

The creation of a Non-Operating Financial Holding Company (NoFHC) to hold the bank’s shares.

5. Why does RBI require a NoFHC?

The NoFHC ensures separation between ownership and banking operations, reducing conflicts of interest and improving governance.

6. How much time has RBI given AU SFB to comply?

AU SFB has 18 months from the date of approval to complete the NoFHC setup and other structural changes.

7. Can AU SFB operate as a universal bank immediately?

No, it will continue as an SFB until all compliance steps are completed.

8. When was the last universal bank licence issued in India?

Over a decade ago, making AU SFB’s case unique in the current regulatory climate.

9. Which RBI guidelines govern this transition?

The Guidelines for Licensing of Universal Banks and RBI’s NoFHC framework for private sector banks.

10. Will AU SFB’s head office remain in Jaipur after the transition?

There is no RBI mandate to shift headquarters, so it can remain in Jaipur unless the bank decides otherwise.

B. Compliance & Governance

11. What is the role of a Non-Operating Financial Holding Company (NoFHC)?

It acts as the parent company holding shares of the bank and its financial subsidiaries, without engaging in any commercial banking itself.

12. Who will own the NoFHC in AU’s case?

The promoters, including MD Sanjay Agarwal, will shift their shareholding from the bank to the NoFHC.

13. Will this transition have tax implications?

Yes, but there are regulatory provisions to waive certain taxes for regulator-mandated corporate restructuring.

14. Does AU need RBI’s approval for the rebranding?

Yes, any change in the bank’s name requires RBI’s approval along with compliance with Companies Act naming rules.

15. Will the board structure change after becoming a universal bank?

It may require changes to meet corporate governance norms applicable to universal banks.

16. Are there any capital adequacy changes required?

The bank must maintain CRAR as per universal bank norms, which may be higher depending on asset profile.

17. Will there be additional compliance reporting?

Yes, universal banks have broader reporting obligations under RBI’s master directions.

18. What happens if AU fails to meet the compliance deadline?

The in-principle approval may lapse, requiring a fresh application.

19. Does AU need SEBI or IRDAI licences as part of this process?

Not for banking, but for offering investment or insurance products, it may require respective regulatory approvals.

20. Will AU’s deposit insurance coverage change?

No, deposits will continue to be insured by DICGC up to ₹5 lakh per depositor.

C. Financial Strategy

21. How will universal bank status affect AU’s cost of funds?

It is expected to lower the cost of funds, as universal banks generally mobilise deposits at lower rates.

22. What is AU’s target for cost of funds?

To bring it below the repo rate within five years.

23. How does AU plan to achieve this?

By improving brand trust, expanding its customer base, and aligning deposit rates with larger banks.

24. Will lending rates change after the transition?

Likely yes, as lower funding costs will allow competitive lending rates.

25. What is AU’s current loan portfolio mix?

Predominantly secured loans, with ~8% in unsecured lending.

26. What is the target for unsecured loans?

Around 15% of the portfolio in the medium term.

27. Why increase unsecured loans?

To diversify revenue and capture higher-yield opportunities while balancing risk.

28. Will yields on advances decrease?

Yes, as competition and diversified lending reduce average yields.

29. How will NIM be maintained?

By balancing lower yields with reduced cost of funds and improved efficiency.

30. What is AU’s ROA target post-transition?

Around 2% in the long run.

D. Strategic Outlook

31. Why rebrand to AU Bank Limited?

To simplify public understanding and remove misconceptions about “small finance” status.

32. How will this help deposit mobilisation?

By increasing depositor trust, enabling lower rates, and expanding the customer base.

33. Will AU compete directly with large private banks?

Partially, but its main competition remains NBFCs in certain secured lending markets.

34. What new products can AU offer as a universal bank?

Expanded credit card offerings, personal loans, corporate banking, and more complex trade finance.

35. Will branch expansion be part of the strategy?

Yes, to increase reach in both urban and semi-urban markets.

36. How will rural customers benefit?

They will have access to more services under one bank brand, without needing multiple financial providers.

37. Will AU continue its focus on secured lending?

Yes, secured lending remains core to its risk strategy.

38. Will AU enter investment banking?

Possible in the future, but not part of immediate transition plans.

39. Will there be digital-first initiatives?

Yes, AU is expected to enhance mobile and online banking platforms.

40. Does AU plan to expand internationally?

Not in the short term; focus remains on domestic market growth.

E. Customer Impact

41. Will existing account holders need to change account numbers?

No, unless system migration during rebranding requires technical changes.

42. Will interest rates on deposits change?

They may gradually align closer to universal bank rates.

43. Will loan EMIs change?

Only if lending rates are revised as part of the new pricing strategy.

44. Will services become more expensive?

Not necessarily; competition could keep fees competitive.

45. Will customers need to submit fresh KYC?

No, unless mandated by RBI as part of compliance updates.

46. Will digital banking apps change?

The app may be rebranded and upgraded, but functionality will remain.

47. Will AU still serve micro and small businesses?

Yes, MSME financing remains a core segment.

48. Will customers get more investment options?

Yes, AU can expand offerings in mutual funds, insurance, and bonds.

49. Will rural banking products be reduced?

No, AU intends to keep rural and semi-urban focus.

50. How will universal bank status benefit customers overall?

By offering wider services, better trust, competitive rates, and a stronger brand.

Why Small Finance Banks Are Not Applying for Universal Banking Licences Yet

‘Small’ isn’t beautiful for small finance banks.

Branded Disclaimer – Estabizz Fintech AU Small Finance Bank Universal Bank Transition

Disclaimer: This article has been prepared by Estabizz Fintech Private Limited for general informational purposes based on publicly available data and RBI guidelines. It does not constitute legal, tax, or investment advice. Banking regulations and licensing norms are subject to change, and readers should consult qualified professionals before making strategic or compliance decisions. Estabizz Fintech shall not be liable for any loss arising from reliance on this content.