Income Tax Filing FY 2024–25: Who Should File ITR-2 and ITR-3 Why It Matters

ITR-2 and ITR-3 Explained: Who Should File and Why It’s Critical in FY 2024–25

Overview

As the income tax return (ITR) filing deadline for FY 2024–25 approaches, choosing the correct ITR form is critical for avoiding scrutiny, penalties, or rejections. While most salaried taxpayers use ITR-1 or ITR-4, those with capital gains, multiple properties, foreign assets, or business/professional income need to use more detailed forms—ITR-2 or ITR-3. Let’s break down what these forms are, who should use them, and why timely compliance is essential.

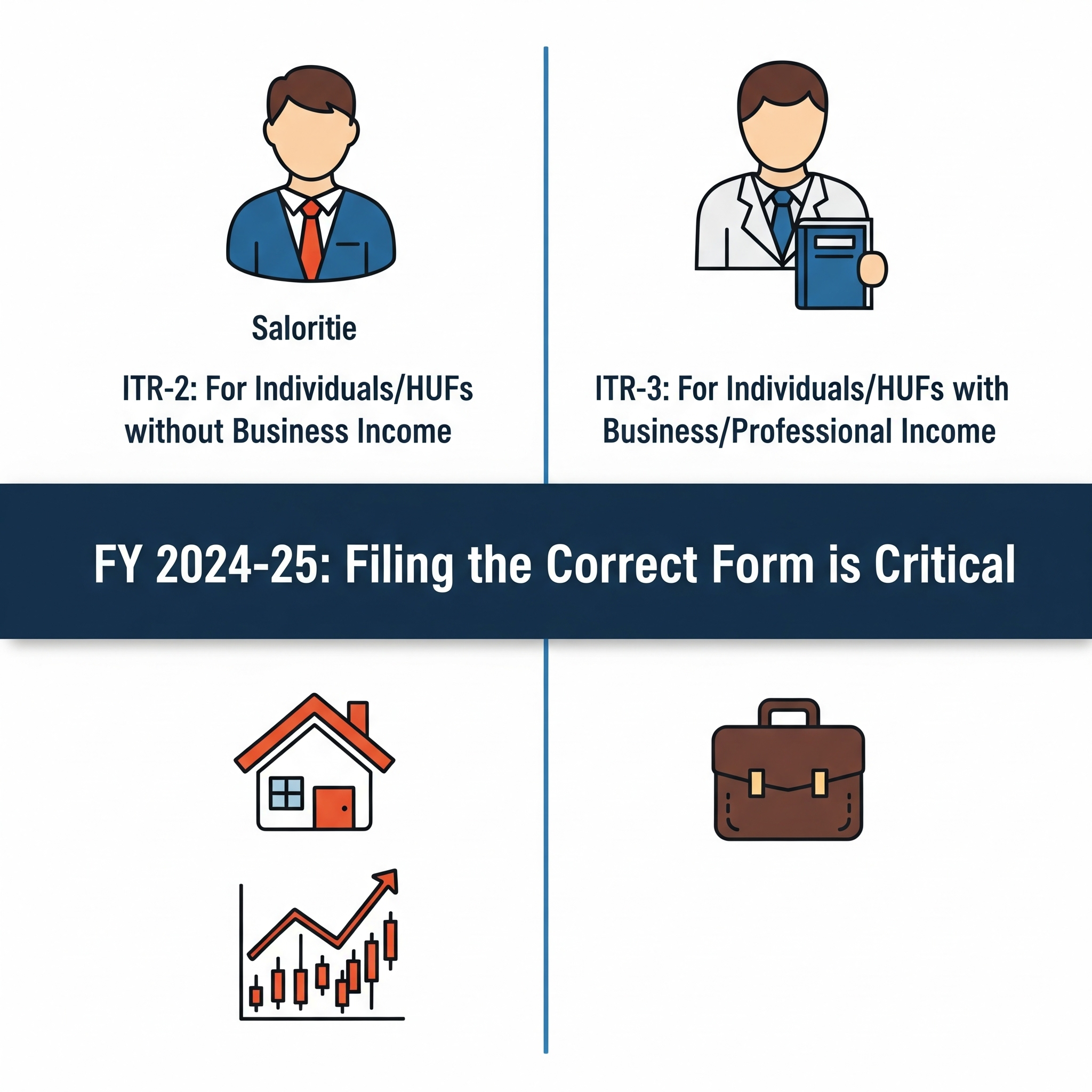

What Is ITR-2 and Who Should File It?

ITR-2 is designed for:

- Individuals or Hindu Undivided Families (HUFs) not having income from business or profession.

- Taxpayers with:

- Capital gains/losses (short-term or long-term)

- More than one house property

- Foreign income or foreign assets

- Income from agriculture exceeding ₹5,000

- Director position in a company or holding unlisted equity shares

- Individuals whose income is not eligible for ITR-1, but do not engage in business.

Use Case Examples:

- A salaried employee earning capital gains from mutual funds.

- An individual earning rental income from two properties.

- A resident Indian with a bank account abroad or foreign stocks.

What Is ITR-3 and Who Should File It?

ITR-3 is for:

- Individuals and HUFs who earn income from a proprietary business or profession.

- Professionals like doctors, lawyers, architects, chartered accountants, and consultants.

- Freelancers and gig economy earners who maintain books of accounts.

- Individuals with income from business or profession along with capital gains or other sources.

Key Indicators for ITR-3 Eligibility:

- You are self-employed or earn consulting income.

- You are a partner in a firm (but not drawing salary from it).

- You’re using actual profit and loss records for computing tax.

Why Choosing the Correct Form Matters

Using the wrong ITR form can lead to:

- Invalid return filing: Treated as not filed, triggering penalties.

- Loss of deductions or exemptions.

- Delays in refunds or IT notices.

More importantly, the ITR forms now include pre-filled data for bank accounts, salary, capital gains, and mutual fund investments, making accuracy and transparency crucial.

What If You Have Multiple Sources of Income?

If your income profile includes:

- Salary + capital gains = ITR-2

- Business income + capital gains = ITR-3

- Freelance income = ITR-3

- Foreign assets = ITR-2 (or ITR-3, depending on business/profession)

Always assess your primary source of income and additional disclosures to determine the right form.

Status of Utilities for FY 2024–25

As of June 2025:

- Excel and JSON utilities for ITR-1 (Sahaj) and ITR-4 (Sugam) are already live.

- ITR-2 and ITR-3 utilities are expected soon, with online filing portals updated periodically by the Income Tax Department.

Deadline & Filing Advice

The due date to file ITR for individuals (non-audit cases) is 31st July 2025, unless extended. Filing early gives you ample time to:

- Validate income data

- Avoid last-minute errors

- Plan taxes if eligible for revised returns under Section 139(5)

🧾 ITR Filing Deadline & Utility Availability

Taxpayers have until 31 July 2025 (for most individuals not subject to audit) to file their returns. While the Excel utility for ITR-1 (Sahaj) and ITR-4 (Sugam) has already been enabled by the Income Tax Department, the online utilities for ITR-2 and ITR-3 are still pending. Many salaried and professional taxpayers are urging the government to enable them soon.

🔍 What is ITR-2?

ITR-2 is for:

Individuals and Hindu Undivided Families (HUFs) not having income from business or profession. This form covers those with income from:

- Salary or pension

- Multiple house properties

- Capital gains (short-term or long-term)

- Foreign income or foreign assets

- Agricultural income exceeding ₹5,000

- Dividend income

- Resident Not Ordinarily Resident (RNOR) or Non-Resident Indians (NRIs)

- Clubbed income of spouse/minor child (if within allowable categories)

When NOT to file ITR-2:

You should not use ITR-2 if you:

- Have income from business/profession (other than salary)

- Are a partner drawing remuneration from a firm

- Are eligible for presumptive taxation (then use ITR-4)

📌 Key Note: If you’re investing in foreign stocks, own property abroad, or have capital gains from shares or mutual funds, ITR-2 is mandatory—even if you’re salaried.

🧾 What is ITR-3?

ITR-3 is designed for:

Individuals or HUFs who earn income from a proprietary business or professional service, and maintain books of accounts. This includes:

- Doctors, lawyers, chartered accountants

- Freelancers or consultants with high turnover

- Partners in firms drawing salary, interest, bonus or profit share

- Traders, retailers, or manufacturers not under presumptive scheme

When NOT to file ITR-3:

- If you are eligible under Section 44AD/ADA/AE for presumptive taxation → use ITR-4

- If your only income is from salary, capital gains, or house property → use ITR-1 or ITR-2 accordingly

📌 Real-world Use Case:

If you’re a software consultant earning ₹25L per annum and managing clients independently (not on salary), you must file ITR-3, disclose books of accounts, and pay advance tax quarterly.

🆚 ITR-1 (Sahaj) and ITR-4 (Sugam) vs ITR-2 and ITR-3

| Criteria | ITR-1 (Sahaj) | ITR-4 (Sugam) | ITR-2 | ITR-3 |

|---|---|---|---|---|

| Salary/Pension | ✅ | ✅ | ✅ | ✅ |

| One House Property | ✅ | ✅ | ✅ | ✅ |

| Multiple House Properties | ❌ | ❌ | ✅ | ✅ |

| Capital Gains Income | ❌ | ❌ | ✅ | ✅ |

| Business/Professional Income | ❌ | ✅ (Presumptive only) | ❌ | ✅ |

| Foreign Assets/Income | ❌ | ❌ | ✅ | ✅ |

| Partner in Firm | ❌ | ❌ | ❌ | ✅ |

| Agricultural Income > ₹5,000 | ❌ | ❌ | ✅ | ✅ |

| Total Income < ₹50 Lakh | ✅ | ✅ | ✅/❌ depending on sources | ✅ |

✅ How to Know Which ITR Form is Right for You?

| Income Source | ITR Form |

| Salary, one house property, no capital gains, income < ₹50L | ITR-1 (Sahaj) |

| Capital gains, foreign income, more than one house | ITR-2 |

| Freelancers, professionals, partners in a firm | ITR-3 |

| Presumptive income scheme (small businesses) | ITR-4 (Sugam) |

🧠 Why Form Selection Matters

Choosing the correct ITR form ensures:

- Faster refunds

- Lower chances of notice or scrutiny

- Compliance with disclosures, especially for capital gains and foreign holdings

- Eligibility for loss set-offs and carry-forward of capital losses

💡 Tip: Filing ITR-2 or ITR-3 also allows more flexibility in claiming exemptions, deductions, and reporting complex financial scenarios.

🕒 Latest Update: Filing Deadline and Utility Access

- ITR Deadline for AY 2025–26: 31 July 2025 (for individuals not subject to tax audit)

- Current Utility Status (as of June 2025):

- ✅ ITR-1 and ITR-4: Excel + JSON utility enabled

- ⏳ ITR-2 and ITR-3: Excel utility pending; JSON (online) expected soon

⚠️ Disclaimer

This content is provided for general informational purposes only and should not be considered as tax advice. Tax rules and forms are subject to change based on notifications by the Income Tax Department. Please consult a certified tax consultant, CA, or legal advisor before making any tax-related decisions. Estabizz Fintech does not assume liability for actions taken based on this content.

Should you report foreign stocks in ITR as per calendar year?